It could be the pebble that create an avalanche

One of the financial items that have been prevalent in the news over the past few years is the exploding level of U.S. student loan debt. The situation has amplified recently, as unemployment increased dramatically and has stayed stubbornly high as the economy continues its anemic recovery. All told, the total balance of student loans outstanding is at approximately $900 billion dollars, and is rapidly approaching $1 Trillion. This is important, because student loan debt cannot be discharged in bankruptcy. People who owe large amounts of student loan debt do not have an easy way out of paying.

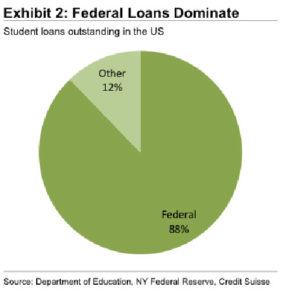

Now consider that the Federal Government owns 88% of all student loans, after acquiring FFEL loans in 2010. Considering that the rate of interest on direct, subsidized student loans after 7/1/12 is 6.8%, and the ten year treasury yield is standing at approximately 1.5%. This means that the government currently clears a spread of over 4% on all student loans it subsidizes. (Assuming that those loans don’t default)

Now consider that the Federal Government owns 88% of all student loans, after acquiring FFEL loans in 2010. Considering that the rate of interest on direct, subsidized student loans after 7/1/12 is 6.8%, and the ten year treasury yield is standing at approximately 1.5%. This means that the government currently clears a spread of over 4% on all student loans it subsidizes. (Assuming that those loans don’t default)

The breadth and scope of the student loan bubble is even more dangerous when one considers that student debt is the fastest growing category of consumer debt. Since this debt cannot be discharged through bankruptcy, the growth of these loans creates a shift in people’s cred profiles toward debt that MUST be paid back.

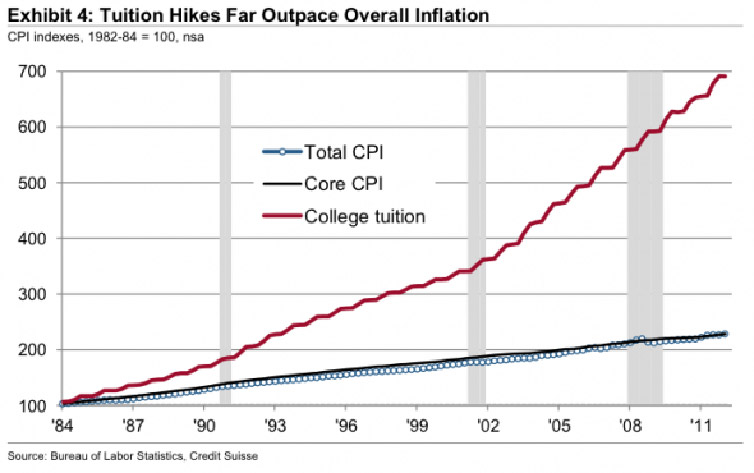

Additionally, the trends show that the severity of this debt bubble will continue to expand. The past 28 years have seen the rate of college tuition increase at approximately three times the rate of the consumer price index. This means that the cost of student loan debt is escalating precipitously at exactly the time when the economy has become terminally soft and graduating students are ill able to take on the repayment of the debt that they have accrued in the pursuit of their degree.

What all of this adds up to is the necessary conditions for a precipitous collapse. The government is currently raking in considerable revenue streams from the student loan business, due to the incredible rate spread between student loans and treasuries. Effectively, the government can borrow for somewhere between zero and 2.5% interest and loan it out at 6.8% interest. Of course, there is a hitch to this apparent gold mine of easy money …

The unbelievably low interest rates of the current time are not going to last indefinitely. With the rapid rate at which the Federal Reserve is printing money, it is only a matter of time before inflation hits and forces up the yield on treasury notes. As the “spread” between the fixed rate student loans and the yield on treasuries shrinks, the government will lose its gravy train, and could eventually be subsidizing a substantial loss on these loans. As these inevitable losses mount, it will place considerable pressure on the government to reduce the rate at which they subsidize student loans. One way that this could be accomplished is through a higher rate on new loans … another way is through increasing the rate of interest charged for existing loans.

The extended impact of this massive student loan debt bubble combined with the looming fiscal cliff that the government is rapidly approaching results in a seismic reduction in the expected future standard of living for an entire generation of Americans. It is not possible to iterate the impact of being unable to discharge student loan debt on the future finances of Americans. The specter of this debt will linger indefinitely. It will create a permanent drain on the disposable income of millions upon millions of people, even under the best of circumstances. In the event that worsening government finances trigger drastic action, the impact could be even more severe.

What this means for us as investors is that there will be a wave of people in the future who have a significantly diminished amount of buying power. This will transpire as a “hollowing out” of the middle class that places a pinch on the products, services, and investments typically purchased by these people. It means that they will rent for longer before becoming homeowners (if they become homeowners at all), they will drive their cars for longer, will buy fewer new cars, will go shopping less, and will invest less into their retirement plans.

As income property investors, the most prevalent impact of this phenomenon is that the housing market will steadily shift from being dominated by owners to an increased prevalence of renters. This will create a continual wave of renters in the marketplace as the people who would normally purchase a home are forced to continue renting, due to their lack of income and assets. This will place upward pressure on rents, and can directly benefit people who purchase prudent income properties and secure today’s low rates of financing.

The student loan bubble is real, and it’s not going away. None of us have the power to stop this hollowing out of the middle class, but we do have the power to place ourselves in a situation to provide the services that will be necessary to support the diminished affluence of future generations.

Action Item: Take advantage of today’s low interest rates to invest in prudent income properties. It may be the best way to defend yourself against the extended impact of the student loan bubble as it ripples out to the broader economy.

Want to read more about national debt? Click here.