Inflation-induced debt destruction is perhaps the most important topic in mortgage financing. Yet it’s the least talked-about. This could explain why millennial home ownership is so low. They just haven’t yet seen the effects of inflation-induced debt destruction.

Let’s look at the connections between housing and inflation by generation. The question here is simple: Which generation has seen the effects of an inflation-induced debt destruction the most?

Some Demographic Background

First, before getting into inflation, here’s a look at the six living generations.

The largest generation now is Generation Z – known as the Boomlets. This represents anyone born from 2000 to today. That’s 19 years and 76 million births. The oldest Boomlet is just now getting through their first year of college. The first batch of Boomlets are perhaps four or five years away from first entering the housing market.

The next largest generation is the Millennials at 72 million births. This captures anyone born between 1981 and 1999. The oldest Millennials are approaching 38 years of age. The youngest will be turning 20 in 2019.

The next largest generations are the Baby Boomers and Generation X. About a third of Baby Boomers – anyone between the ages of 55 and 71, are now into their retirement.

On to Inflation-Induced Debt Destruction

With generation divides established, let’s switch back to the main question. Have Millennials seen the effects of inflation-induced debt destruction yet?

Here’s the answer.

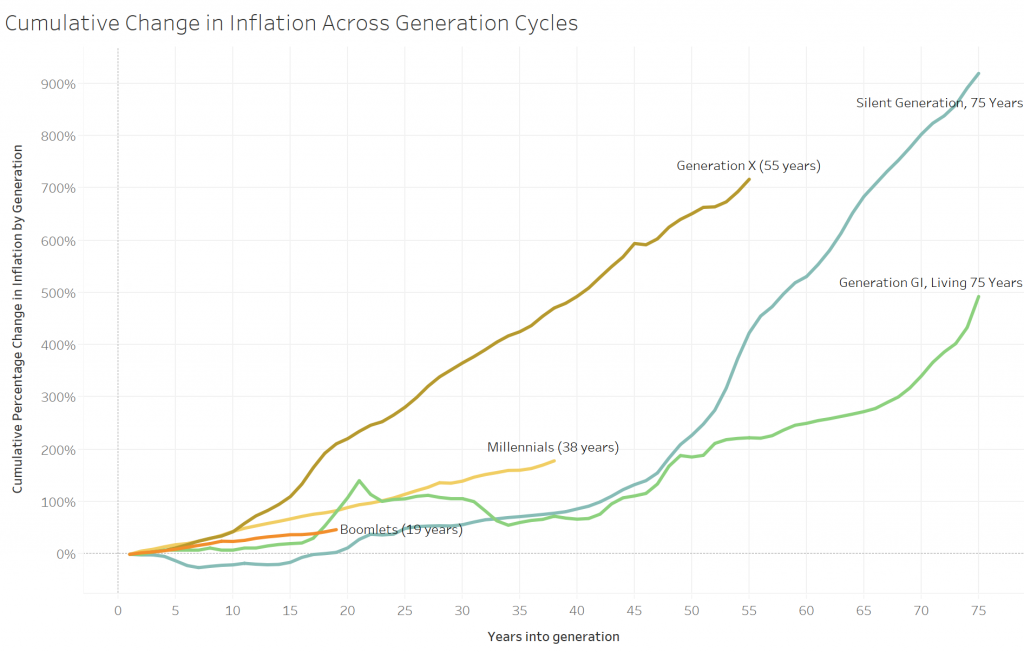

The coming chart is inflation across the generations. The figure shows 75 years for generations that have been alive that long.

Overall, the Silent Generation, the one that began in 1900, saw inflation explode by around 950%. That’s 950% over the life of an individual born in 1900 and living until 1975.

By contrast, Generation GI only saw inflation of 500%. Generation X, the oldest member of which is now 55 years, has seen inflation of just over 700%.

What about the two recent generations? They haven’t seen an explosion in inflation, at least not yet. Over the 38 years of the first Millennial, inflation has expanded by about 179%. The Boomlets, at 19 years and counting, have seen inflation expand by 47%.

If inflation-induced debt destruction helps borrowers, Millennials just haven’t seen that much of it compared to the generation before them.

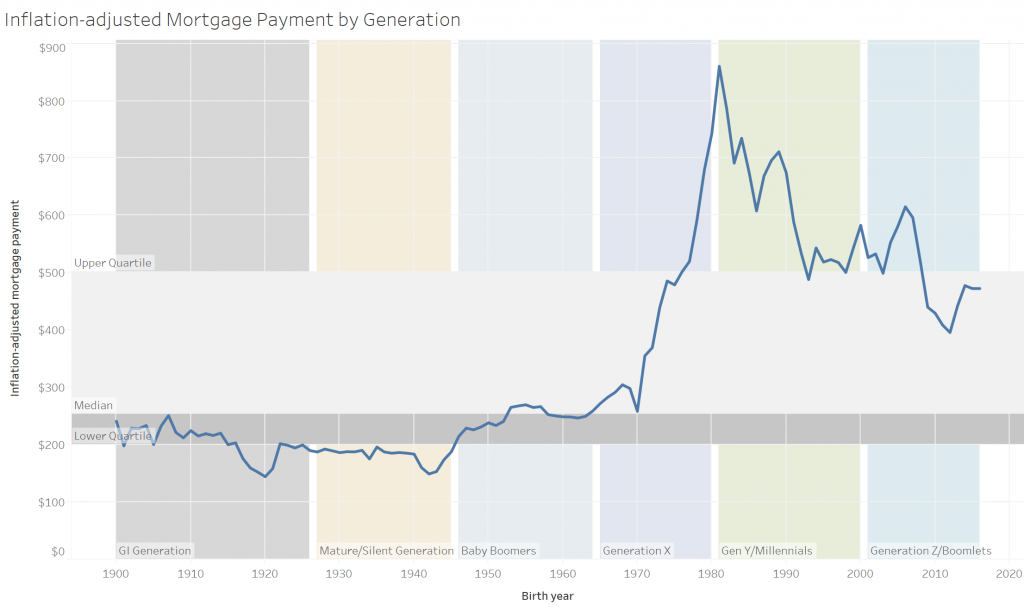

Switching to Inflation and the 30-Year Mortgage Payment

Inflation eats away at a mortgage payment. Have Millennials seen their inflation-adjusted mortgage payment decline much? The answer is no. Could this be why millennial home ownership is down? Probably.

Here’s a look, by generation, at the mortgage payment adjusted for inflation. Unsurprisingly, the Millennial generation has the highest mortgage payment of all the previous generations. That’s even after accounting for the early 80s hyperinflation.

Source: Calculations by Econometric Studios based upon data from the BLS, the Federal Housing Finance Agency, Robert Shiller, National Association of Home Builders

Conclusion

Overall, Millennials just haven’t seen big inflation yet. Because of this, inflation-induced debt destruction is more of a concept than a reality to them. Perhaps this explains the lower millennial home ownership rates.

Looking for more home ownership stats? Read Homeownership Statistics 2019