It is well known the United States has a major national debt problem. Every time the US national debt adds another trillion dollars to its total, a fresh series of news stories are published to warn of impending peril. However, many have noted that the forecasted problems have not yet come to pass. The economy is still growing, and interest rates remain at historically low levels.

In short, the old mantra of chickens coming home to roost does not seem to hold true. The United States keeps increasing the debt it owes to its citizens and the rest of the world with no ill effect.

One can almost say (wait for it) … “This time it’s different.”

Financial Gravity

It’s tempting to believe that debt obligations can be continually increased without consequences, but the simple fact of the matter is that nobody can escape ‘financial gravity.’ The gravity we are talking about in this case is: Interest must be paid on debts or else loans will eventually cease. This is where the problems start.

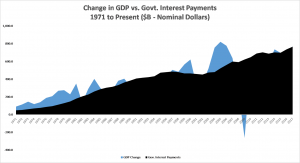

Looking at a chart of the US nominal growth in Gross Domestic Product since 1971, overlayed against a similar chart of the debt payments owed by the US government shows a grim picture. (Figure 1) To fully understand this picture, we must first outline the difference between “nominal” and “adjusted” numbers. The “nominal” GDP growth represents the total dollar growth in economic output without adjusting for inflation. The reason we look at nominal GDP growth is because we must compare it against nominal interest payments. Put another way, we’d rather compare apples to apples.

At this point, you might ask why we do not index the numbers for inflation and show “real” numbers. Inflation has an extremely high impact on people’s cost of living and quality of life, but is not a necessary component of the analysis we are conducting. Ultimately, we are asking a simple question: “Is the economy growing fast enough to pay the interest on the US debt?”

The short answer is ‘not anymore.’

Throughout the 1970s, economic growth continually outpaced interest payments on the national debt. In the 1980’s this began to change. Actions taken by the Federal Reserve to fight inflation resulted in growth that failed to keep pace with interest payments, leading to a major recession by 1982. From there, the economy recovered, even boomed for a period in the mid-1980s, and again fell into recession by the early 1990s. The economy rebounded during the mid-to-late-1990s, until the expanding dot-com bubble crashed. Then the real estate bubble dramatically expanded and crashed, as the Great Recession hit in 2008, and GDP growth has not kept pace with interest payments since then.

What This Tells US National Debt

The key insight we can take away from this information is that the US cannot grow its way out of the national debt problem. Prevailing economic theory had been that if the economy grows fast enough, the debt problem would dissipate over time. Unfortunately, the situational mathematics make it highly unlikely the US can grow its economy rapidly enough to address the debt problem without major changes to government entitlements, raising taxes, or by monetizing the debt and causing inflation.

The reason the US is unable to accomplish this feat is because the annual growth in government debt has exceeded the annual growth in GDP since 2007. What this tells us is that debt-based government spending is what has kept the economy growing. The only way to reverse the trend is if a sudden surge of private sector economic growth emerges, with no connection to government funding.

One can hope for such an occurrence, but hope alone is a poor strategy.

In my next article, I will explore the impact of changes in the effective interest rate the US government must pay on its debt, and the impact it will have on both the economy and individuals.

Want to know more about inflation and debt? Read – Millennials Haven’t Really Seen the Effects of Inflation-Induced Debt Destruction – Yet